Still Looking For a Fast and Easy Way to Manage

Your Personal or Family Household Cashflow?

Hi, I’m Lee Roesner,

Creator of MoneySlinger

I’ve got a system so efficient and fast,

that I can afford to manage your money for you…

For Free.

Could It Get Any Faster and Easier Than That?

I don’t think so.

No, I’m Not Crazy

And no, this is not a scam.

Because I won’t be managing your

money ~ for free or otherwise.

But I wanted you to sense

for a moment, how fast and easy,

fast and easy can be.

Because this level of fast and easy

is my benchmark offer to you, and

why you should take a moment

to read a bit further.

This is legit…I live and have a Graphic Design

business in Northern Illinois just outside Chicago.

You can check out my Graphic Design Business which

I’ve run for some 19 years or my Linkedin Profile.

Take note of the recommendations.

You see, this offer may be free to you,

but I can make some good money from other

sources that are betting you can’t manage

your money well.

So I’ll plan and manage your personal

or family finances, while also paying your bills on

time, all while you save tons of time and enjoy

an effortless FICO score above 800.

Still Think There’s a Catch?

You see, I’m a lazy perfectionist, a creative

and a bit of an inventor, and like you,

my time is precious

not to mention my money.

In 1988, I ended up “unknowingly” cracking

this nut like no one else has. I say unknowingly,

because we used it for 15 years not knowing what

we did ~ because we did so little ~ while effortlessly

maintaining a FICO score over 820.

As a matter of fact, still not knowing

what we had, I attempted to dump it

after 15 years for a bright, shiny and new

“real” money management software package.

That’s when the lights went on.

This is how I began making fun of the

whole money management industry, because

I’ve come to find out most everyone

is just plain stuck in an old paradigm

which is little more than an elaborate

checkbook balancing exercise.

Most can’t see the forest through the trees,

even if you put a picture of the forest in front of them.

But there are a few who come to see the light

made self evident by the testimonials on

the right side of this page.

So, the catch…(if you want to call it that)

is if you were to allow me to plan and manage

your personal or family finances, is you need to meet

one requirement on your end ~ and for two reasons:

I won’t be paying your bills

on your schedule ~ but on mine.

And of course I won’t be paying them

with my money ~ but with yours.

Here’s What I’ll Need You To Do

(click tab to see details)

So What’s Your Responsibility In This Deal?

If you’ve read the details of what’s required above,

you’ll know that I’ll end up managing approximately

80% of your entire cashflow volume.

Your only money management responsibility now

is to contribute the SAME amount to me

on the SAME two dates each month

~ I’ll take care of the rest.

Is that fast and easy enough?

Your 2 identical payments ~ made on 2 identical dates

essentially pay every one of your numerous individual

expenses each month and will take care of some 80% or

more of your most important life expenses.

Could it get any easier?

Well, actually it can.

How About That Other 20%?

That other 20% is what you’ll be managing,

but that 20% is not just any percent.

It’s a balance…and that balance is

the difference between what you earned

that pay period, and your average monthly

expense you’re paying me to cover

all your “must have” expenses.

Which means, if you have variable income,

that 20% is sometimes 10%, or 15%…or 25%

~ it’s whatever’s left.

It also means this balance is sitting

all by its lonesome self in its own bank

account, physically separated from

your “must have” money.

Which also means when you open

up your daily checkbook or look at your

online bank account, that “must have”

money is not there either

~ just whatever’s left.

Which means the only daily

“budgeting” or “tracking” you’ll have to

do is to make sure you don’t run out

of money before your next pay period

~ where you’ll pay me first.

I think that’s about it.

Everything else is taken care of.

Really. Think about it.

What else is there?

It makes for easy daily decision

making on your end, doesn’t it?

What Will I Be Doing?

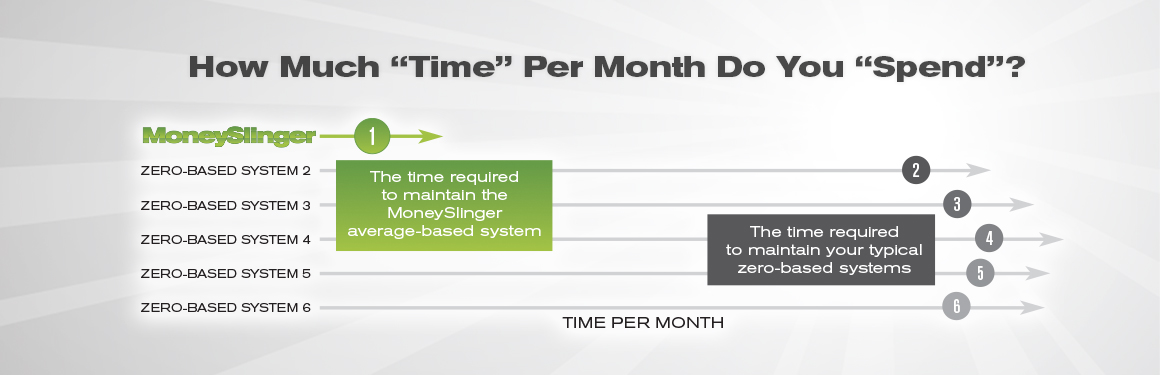

Being the lazy perfectionist I am, I’ll

be doing as little as possible ~ perfectly.

Fortunately, I have a little program I

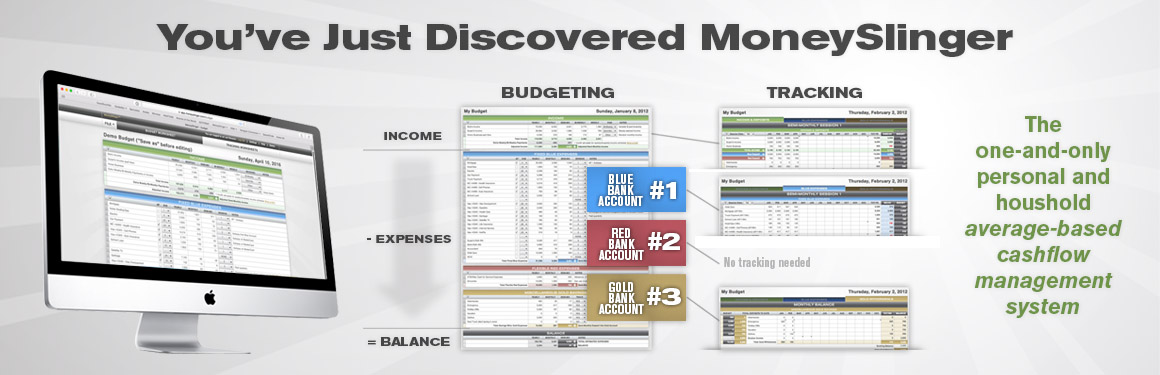

developed around mathematical averaging.

As a matter of fact it has a Budget Worksheet

that does for you, what you just manually did above

that determines your payment amount to me.

It also has a Deposit Tracking Worksheet that tracks

your income; that then subtracts that deposit payment

to me; which determines the deposit balance to you.

But key to my task, is the Expense

Worksheet where I track only the

“must have” expenses you’ve determined you

must financially meet in your life.

But, it does a bit more than just track each

expense payment made each month, it

continually calculates a monthly running average

for each through the year, and compares this

“actual” running average side-by-side

next to the “estimated” average

you determined earlier.

I should also mention it has a

Savings Worksheet as well should you

decide to dedicate some of your money for

future goals that may be a little more long term.

I can handle that for you as well.

And I think that’s it.

No, There’s More

Or should I say, less?

If you recall, your deposit to me will be

deposited in your own, dedicated bank

account in your name.

And I forgot to mention above, that

the Expense Tracking Worksheet not only

calculates a running average through the

year for each individual expense,

it also totals all these individual payouts

into a single monthly “actual” average, and

compares it to the “estimated” deposit

payment you’re making to me.

Still with me?

You see, the thing about averaging

when used in combination with a dedicated bank

account, is all the variability of individual monthly

expense amounts you normally have to contend

with ~ actually cancel each other out.

That’s to say, if one payment is higher than

your average estimate in a particular month, it’s

compensated for in the bank account by another expense

payment that is under your average estimate.

The more variable items you put into this

dedicated account, the less variabilty there is

in the actual balance of the account.

Get it?

So while I may be tracking your individual

expenses, it’s now OK if they float over and under

your average estimate in a particular month,

(to a particular degree of course).

What becomes important then, is not so

much each individual expense figure

~ but your total average expense.

And so my financial focus on our account

is not on the trees, but is on the forest

~ which is a single figure.

Get it more?

So even if some of your expenses are

seasonly variable, your deposit stays

the same all year long.

So the money you may payout in say, summer,

that is “under” your estimated annual average

accumulates in the dedicated

bank account, and is there in winter when

your average payout is “higher” than

your annual average.

Are you getting how easy my job is?

Well, It Gets Easier

Yea, can you believe it?

You have to remember, your

semi-monthly deposit to me is

essentially “payment in full”

for each half month’s expenses.

What this means is not only is your

personal calculation effort at near zero

each month, by simply balancing your

checkbook, but my own calculation

efforts are at near zero as well.

What’s to calculate?

What’s to decide?

There is only to track and confirm.

So my job now is to lighten my

administrative load even more and to automate

my payment process as much as possible.

That means I’ll set up as many autopayments

as I may want because I am 100% sure there

is money in the bank account to cover them.

(Remember we still have the

10% cushion in the account as well)

So How Do I Make Money?

I setup the autopayments using

my own credit card. Not only am I sure I

can pay it off in full with your deposit when

it’s due…but I’ll gain all the free points

and prizes and beat the credit card

companies at their own game.

If you don’t mind.

(note: not sure how to close yet…)